We're here to help you get your life back on track.

For People In Solano County As Well As Its Surrounding Areas, It Has An Easy And Quick Credit Remedy Through Solano Credit Repair. For Those Of You That Have Run Into Difficulty Using Their Credit Situation, Our Professionals Are Available For A Primary Credit Complimentary Consultation. When Credit Issues Arise, It Takes A Trained Expert To Assess The Situation And Apply The Credit Restoration Procedures. Our Personnel Here At Solano Credit Satisfies The Necessary Criteria To Bring Back Your Credit Rating.

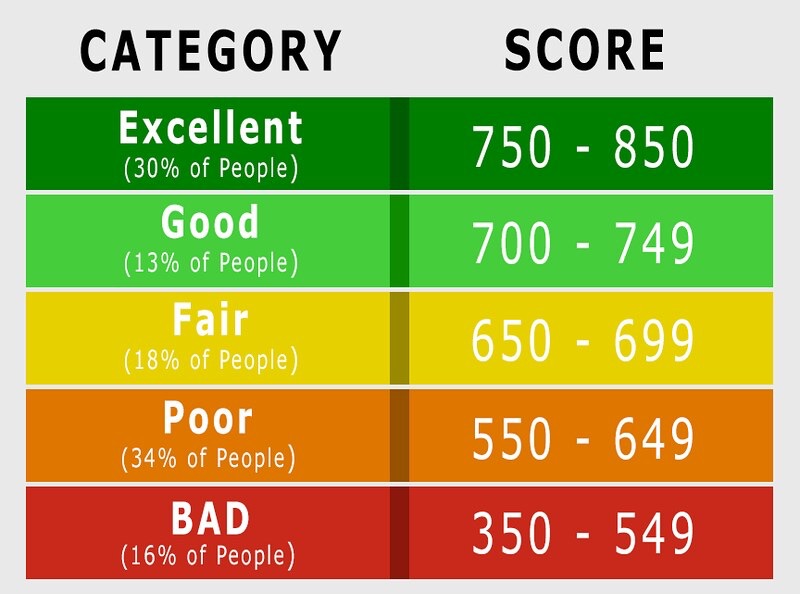

There Are All Kinds Of Credit Issues That May Arise That Harm Your Credit Rating. A Few Of The Credit Issues That Solano Credit Repair Happen To Be Successful With Tend To Be Those Arising From, Determine Theft Or Unfavorable Remarks Appearing Upon Wrong Credit Reports. In Addition To This Our Professionals Can Find The Credit Options For Student Loans Or Even Debt Settlement Issues. Dealing With A Credit Score Issue Related To Late Payments, Or Conclusions, And Even Collections As Well As Bankruptcy Our Team Associated With Professionals Can Help. Figures Play An Important Part In Your Life And One Group Of Numbers That Can Impact Your Future Would Be The Three Numbers Which Appear On Your Credit Rating. As Mentioned, Our Experienced Credit Repair Specialists Can Find An Appropriate Solution For Many Credit Score Problems, But All Of Us Also Expand Our Services To Include Guidance For Credit As Well As Financial Planning. An Unhealthy Credit Score Not Only Limitations You From Acquiring Financing, But May Also Cost You Thousands Of Dollars. Due To A Poor Credit Rating, You Get Paying Higher Home Loan Interests And Best Interest Dollars On The Credit Cards Or For The Vehicle Loan. Your Car Insurance Along With Other Types Of Borrowing Expenses Can Be Escalated Almost All Because Of Your Poor Credit Rating. Here At Solano Credit Repair, We Have Been Adept At Coping With The Main Credit Bureaus For Example Transunion, Equifax As Well As Experian. Why Not Request Your Free Credit Score Consultation With Us Right Now So You Can Take Which First Step To Becoming A Good Credit Score Risk. We Offer The 100% Money Back Guarantee Upon All Of Our Services. Our Passion To Assisting Our Clients Obtain Poor Credit Relief Is Exactly What Is Making All Of Us The Number One Choice Within The Credit Repair Business. Our Experts Tend To Be 100% Legal Credit Score Restoration Professionals That Are Fico Certified. Knowing And Pro-Active Within Turning You’re The Situation Around Is Paramount To Your Achievement, And Our Solano Credit Repair Group Of Professionals Works With You To Achieve This All The Way. Not Only Will Certainly The End Results Be A Fixed Credit Rating But You Will Have The Power To Keep Your Credit Standing For The Future. When You Become A Client Associated With Solano Credit Repair You Will Have Access To Your File Here 24 / 7, So You Can Receive Communications From Us, As Well As Track The Improvement That Is Being Created By Us On Your Credit History. |

Call now or enter your information for your FREE credit consultation! |

IDENTIFY & CORRECT

CREDIT REPORT ERRORS At Solano credit repair, we work on your behalf, disputing inaccurate credit report items with the credit bureaus and your creditors. We’ve effectively disputed every kind of problem a credit report can have and we’re waiting to help you now.

CREDIT EDUCATION

AND TOOLS With our tools and experience, we help you make the best of your credit. Understanding all the facts of credit and credit repair can be confusing, so we created this education center to make it easier for you.

In today’s world, identity theft is one of the fastest-growing crimes. With our services, we keep you informed of any changes or updates on your credit report and advise you on how the reported items affect your credit.

Debt Avalanche vs the Snowball Effect: Which Payoff Strategy Is Better? By Marketing | Debt The decision to focus your energy on paying off your debt is an incredible step in taking control of your finances. Once you’ve knocked out high-interest debt in particular, you’ll free up your money to then hit even greater goals for things like a down payment on a home, retirement savings, or a vacation.

To be really strategic with the funds you have available for paying down debt, consider choosing between two popular methods: the debt avalanche or the snowball effect. Not sure what those two strategies entail? Keep reading to find out what they mean and which is better for you.

What Is a Debt Avalanche? The debt avalanche method has you prioritize your debts by interest rate. You’ll need to start by finding out all your current APRs across the accounts you want to pay off, including credit cards, loans, and lines of credit. Once you’ve identified the balance with the highest rate, you’ll funnel all your extra debt payments to that account. You’ll still need to make the minimum payments on all your other debt. Any money you can divert to extra payments, however, should be focused on that first balance with the highest interest. Once you knock that one out, you’ll then move on to the debt with the next highest rate.

The single greatest advantage to the debt avalanche strategy is that it saves you the most money in the long run. Because you’re tackling the highest interest rate, you’ll stop paying that APR sooner, regardless of what your balance is. That means you’ll start accruing less debt from a growing principal balance thanks to those high rates. Sometimes the choice might be as obvious as a credit card with an 18 percent APR versus a car payment with a 6 percent APR. Clearly, you’ll save more money if you can get rid of that 18 percent rate faster. If you have multiple credit cards or high-interest personal loans, you may need to do some digging as to which one will save you more over time.

Disadvantages while it makes sense to pay down your biggest APR debt from a financial perspective, it might not be the best move from a moral perspective. It can take longer to get a win depending on how high your balance is from the start. Still, if you can stay motivated, you could end up saving a lot more money throughout your entire debt payoff process.

What Is the Snowball Effect? There are a few key differences when considering a debt avalanche versus the snowball effect for your payoff strategy. The snowball effect has you start by paying off your smallest debt, regardless of how much the interest rate may be. After you pay down that balance, you then move to the next smallest balance.

In the meantime, you’re still paying minimum balances on all your other accounts. As you pay and focus on lower-dollar balances, you gain momentum and confidence in your ability to knock out your debt altogether.

CREDIT REPORT ERRORS At Solano credit repair, we work on your behalf, disputing inaccurate credit report items with the credit bureaus and your creditors. We’ve effectively disputed every kind of problem a credit report can have and we’re waiting to help you now.

CREDIT EDUCATION

AND TOOLS With our tools and experience, we help you make the best of your credit. Understanding all the facts of credit and credit repair can be confusing, so we created this education center to make it easier for you.

In today’s world, identity theft is one of the fastest-growing crimes. With our services, we keep you informed of any changes or updates on your credit report and advise you on how the reported items affect your credit.

Debt Avalanche vs the Snowball Effect: Which Payoff Strategy Is Better? By Marketing | Debt The decision to focus your energy on paying off your debt is an incredible step in taking control of your finances. Once you’ve knocked out high-interest debt in particular, you’ll free up your money to then hit even greater goals for things like a down payment on a home, retirement savings, or a vacation.

To be really strategic with the funds you have available for paying down debt, consider choosing between two popular methods: the debt avalanche or the snowball effect. Not sure what those two strategies entail? Keep reading to find out what they mean and which is better for you.

What Is a Debt Avalanche? The debt avalanche method has you prioritize your debts by interest rate. You’ll need to start by finding out all your current APRs across the accounts you want to pay off, including credit cards, loans, and lines of credit. Once you’ve identified the balance with the highest rate, you’ll funnel all your extra debt payments to that account. You’ll still need to make the minimum payments on all your other debt. Any money you can divert to extra payments, however, should be focused on that first balance with the highest interest. Once you knock that one out, you’ll then move on to the debt with the next highest rate.

The single greatest advantage to the debt avalanche strategy is that it saves you the most money in the long run. Because you’re tackling the highest interest rate, you’ll stop paying that APR sooner, regardless of what your balance is. That means you’ll start accruing less debt from a growing principal balance thanks to those high rates. Sometimes the choice might be as obvious as a credit card with an 18 percent APR versus a car payment with a 6 percent APR. Clearly, you’ll save more money if you can get rid of that 18 percent rate faster. If you have multiple credit cards or high-interest personal loans, you may need to do some digging as to which one will save you more over time.

Disadvantages while it makes sense to pay down your biggest APR debt from a financial perspective, it might not be the best move from a moral perspective. It can take longer to get a win depending on how high your balance is from the start. Still, if you can stay motivated, you could end up saving a lot more money throughout your entire debt payoff process.

What Is the Snowball Effect? There are a few key differences when considering a debt avalanche versus the snowball effect for your payoff strategy. The snowball effect has you start by paying off your smallest debt, regardless of how much the interest rate may be. After you pay down that balance, you then move to the next smallest balance.

In the meantime, you’re still paying minimum balances on all your other accounts. As you pay and focus on lower-dollar balances, you gain momentum and confidence in your ability to knock out your debt altogether.

Here's what a few of our highly satisfied customers had to say about Solano Credit Repair:

|

"I thought I could never get my credit score higher than 600. Thanks to Solano credit repair I now have a score of 792!"

Roland G. Fairfield, CA |

"Not only did Solano credit repair able to fix my credit score, but they also helped me fix my LIFE."

Kris Y. Vacaville, CA |

Before Solano Credit repair, I was never able to travel outside of the U.S. now, I am traveling the world. Thank you SOLANO CREDIT REPAIR!

Greg O. Hercules, CA |